Healthcare-related expenditures have been and continue to be one of the biggest expenditures a retiree will face during their retirement years. According to Fidelity and Health View Services, a healthy individual retiring in 2026 will spend an estimated $315,000 – $415,000 on healthcare-related expenditures during their retirement years. Note that the $315,000 – $415,000 estimated cost does not include the additional cost associated with long-term care.

There are three drivers of rising medical care expenditures that are contributing to the federal retiree’s challenge of paying for health care related expenses in retirement.

Healthcare Inflation Exceeding Cost-of-Living Adjustments for Retirees

The first driver is general healthcare inflation which in the recent past has exceeded the cost-of-living adjustments (COLAs) that Social Security recipients and CSRS and FERS annuitants receive.

READ: 2027 Federal Retiree COLA Estimate

For example, during the years 2023-2025, general healthcare-related costs increased by 7.4 percent, 7.2 percent, and 7.1 percent, respectively. For those three years, the average annual increase in health care expenditures is 7.23 percent. In comparison, in January 2024, CSRS annuitants and Social Security recipients received a COLA of 3.2 percent and FERS annuitants received a COLA of 2.2 percent. In January 2025, CSRS annuitants and Social Security recipients received a COLA of 2.5 percent and FERS annuitants received a COLA of 2.0 percent In January 2026, CSRS annuitants and Social Security recipients received a COLA of 2.8 percent and FERS annuitants received a COLA of 2.0 percent These are examples of three years in which CSRS and FERS annuities and Social Security monthly retirement benefits COLAs did not keep pace with the annual increasing cost of health care.

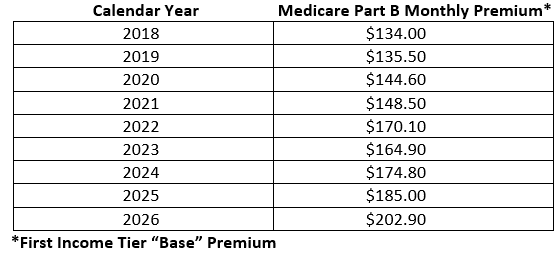

Rising Medicare Part B Premiums

READ: How Federal Employees Can Appeal High Medicare Premiums

Contributing a large part of the 7.23 percent average increase in annual health care-related expenses during the years 2023-2025 is the second driver of rising medical care expenditures, the annual increase in monthly Medicare Part B premiums. Most federal retirees over age 65 and their spouses are enrolled in Medicare Part B (Medical Insurance). Medicare Part B premiums have steadily increased over the years and are projected to continue increasing. This is mainly due to the ever-increasing costs of healthcare services. Medicare Part B premium costs are dependent on a Medicare Part B beneficiary’s annual adjusted gross income, but the “base” premium typically increases each year. The table below shows how Medicare Part B premiums have increased between 2018 and 2026:

Note that the average Medicare Part B monthly premium increase for the period 2023-2025 is 12.19 percent, nearly twice the average increase in annual health care-related expenses during the same period and almost six times the CSRS and FERS COLAs.

While not required, federal retirees when they become age 65 are encouraged to enroll in Medicare Parts A and B. The reason is that between being enrolled in the Federal Employees Health Benefits (FEHB) program and Medicare, a federal retiree will minimize and more likely eliminate any out-of-pocket health-care related expense including deductibles, co-insurance and co-payments for doctor, hospital, and lab bills.

READ: Should Federal Employees & Retirees Enroll in Medicare Part B?

However, federal retirees are fortunate in that they are better prepared and able to pay their health care expenses during their retirement compared to individuals who worked in private industry employment. This is because unlike individuals who worked and retired from private industry employment, federal employees are eligible to keep their Federal Employees Health Benefits (FEHB) group health insurance throughout their retirement in which the federal government pays on average 72 to 75 percent of the federal retiree’s (and spouse’s) FEHB premiums. The federal government’s contribution towards the cost of a retiree’s health insurance premiums throughout retirement can reduce a federal annuitant’s (and spouse’s FEHB premiums if married) expected out-of-pocket health care expenditures during retirement by at least 70 to 80 percent.

But federal employes and retirees also need to be concerned with the cost of future long-term care, the third driver of rising medical care expenditures.

Cost of Long-Term Care

READ: With Average 86% Increase in FLTCIP Premiums, Self-Insuring Long Term Care Becomes a Consideration

The cost of long-term care (LTC) can be expensive and varies greatly depending on the type of LTC (institutional care versus non-institutional care) an individual needs, the place or setting in which the care is provided, and the area of the country in which an individual resides. Planning for possible future LTC expenses can be a challenge. Perhaps the biggest challenge in addressing one’s possible future LTC needs is overcoming the emotional issues LTC raises for individuals and the difficulty in getting a handle on the actual risk of needing prolonged LTC.

Rand Corporation research concluded that 56 percent of individuals between the ages of 57 and 61 will spend at least one night in a nursing home during their lifetimes. These same individuals will have a 10 percent chance of spending three or more years in a nursing home and a 5 percent chance of spending more than four years in a nursing home.

In dollar terms, longer stays in a nursing home can pose a major financial risk. According to Genworth and CareScout 2024 annual cost of LTC survey, in-home caretaker and assisted living community costs increased the most at 10 percent, the increase for most care types continued to outpace inflation.

The Genworth* and CareScout** survey showed the following increase in long- term care costs between 2023 and 2024:

• The cost of a home health care aid, which includes direct personal assistance with activities such as bathing, dressing, and eating, has increased 3 percent to an annual median cost of $77,792. Homemaker services, which include assistance with “hands-off” tasks such as cooking, cleaning, and running errands, have increased 10 percent to an annual median cost of $75,504

Driving the outsized increase in homemaker services is the compression between home health aide and homemaker service rates. Two-thirds of home care agencies surveyed now charge the same rate for both types of service, where the less clinical homemaker tasks historically have demanded lower rates.

• The annual national median cost for adult day care was $26,000, a 5 percent increase over the prior year.

• Assisted living costs increased by 10 percent to an annual national median cost of $70,800 per year. Occupancy rates increased year-over-year, from 77 percent to 84 percent, which may be pressuring supply and driving higher rates.

• The national annual median cost of a semi-private room in a nursing home rose to $111,325, an increase of 7 percent, while the cost of a private room in a nursing home increased 9 percent to $127,750.

Once again, the increase between 2023 and 2024 in LTC services far exceeds the federal retiree COLAs paid during 2023 and 2024.

Fortunately, there are ways for federal employees and retirees to pay for possible future LTC expenses. One way is through LTC insurance. But LTC insurance has never caught on as a widespread solution to the problem of paying future LTC expenses. Only 8 percent of individuals in the US have purchased LTC insurance. Federal employees and retirees are eligible to apply at any time for the federal government-sponsored Federal Long Term Care Insurance Program (FLTCIP) (www.ltcfeds.com). Like many individual and group LTC insurance plans, the FLTCIP has become expensive in recent years. Many employees and retirees who applied for the program in the early years of the program and who were approved for coverage cannot now afford the premiums. Many of these employees and retirees have dropped out of the program. Other employees and retirees who are thinking about applying for it are not because of the rising premium costs or they could not qualify due to medical issues.

Fewer insurance companies offer individual LTC insurance. There are only five to eight insurance companies that offer individual LTC insurance policies. Rising premiums and stricter qualification guidelines have resulted in a decrease in individual LTC insurance policy ownership.

Instead of LTC insurance policy ownership to pay future LTC expenses, federal employees are advised to consider self-insuring to pay future LTC expenses. For example, employees may want to set aside as their “rainy day” LTC account portions of their Thrift Savings Plan (TSP) in case they need those assets to pay for LTC. The Roth TSP is particularly useful because qualified Roth TSP withdrawals are not taxable.

Another source for paying future LTC expenses is home equity. Many employees and retirees own their homes outright (no mortgages). Their home equity can be used to pay for possible LTC expenses. For example, using a reverse mortgage to generate income to pay LTC expenses.

The advantage of self-insuring to pay future LTC expenses is that if a federal employee or retiree does not use all or only a portion of the investment assets set aside to “self-insure,” then at the employee’s or retiree’s death any remaining assets can be passed onto surviving family members.

Federal employees and retirees are also advised to keep in mind possible future LTC costs in determining when to start receiving monthly Social Security retirement benefits. To maximize their monthly Social Security retirement benefit, they should wait until age 70 to start receiving their monthly benefit. Actuarially speaking, any individual who delays until age 70 the start of receiving their monthly Social Security benefit will have to live until at least 82.5 in order to make the wait financially advantageous. This is important because most individuals who incur a need for LTC services will do so starting in their early-to mid-80s.

READ: 10 Ways for Federal Retirees to Maximize Social Security Benefits

*About Genworth Financial

Genworth Financial, Inc (“Genworth”) (NYSE: GNW) is a Fortune 500 company focused on empowering families to navigate the aging journey with confidence, now and in the future. Headquartered in Richmond, Virginia, Genworth and its CareScout businesses provide guidance, products, and services that help people understand their caregiving options and fund their long-term care needs. Genworth is also the parent company and majority-owner of publicly traded Enact Holdings, Inc., a leading U.S. mortgage insurance provider.

**About CareScout

CareScout helps older adults and their families navigate the aging journey and find quality care. Inspired by a mission to simplify and dignify the aging experience, we are building an integrated ecosystem of care and funding solutions. To learn more about CareScout, visit www.CareScout.com. CareScout, LLC (CareScout) is a wholly owned subsidiary of Genworth Financial, Inc.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019