The Roth Thrift Savings Plan (Roth TSP) has become an increasingly popular retirement savings option for federal employees who want the opportunity for tax-free qualified withdrawals in retirement. For many participants, contributing to the Roth TSP is an excellent long-term strategy.

However, a Roth TSP is only one piece of the retirement planning puzzle. A Roth IRA is a separate retirement account governed by different IRS rules. Opening one early — even if you contribute only a modest amount — may provide additional flexibility later in retirement. It can establish the Roth IRA’s five-year aging period, create future rollover opportunities, expand investment choices, and potentially simplify retirement income planning.

This does not mean every federal employee should stop contributing to the TSP or move money out of it. In fact, for most Federal Employees Retirement System (FERS) employees, contributing enough to receive the full government matching contribution should remain a priority.

Instead, many retirement specialists view the Roth TSP and Roth IRA as complementary accounts that can work together throughout a federal career and into retirement.

Key Takeaways

- The Roth TSP and Roth IRA are separate retirement accounts with different rules.

- Opening a Roth IRA starts its own five-year aging period under IRS rules.

- The Roth IRA’s five-year clock is separate from the Roth TSP’s five-year requirement.

- Beginning in 2024, Roth TSP accounts are no longer subject to Required Minimum Distributions (RMDs) while the money remains in the TSP because of changes made by the SECURE 2.0 Act.

- Qualified Roth TSP balances may generally be rolled into a Roth IRA after separating from federal service.

- Roth IRAs typically offer significantly more investment choices than the TSP.

- Many federal employees benefit from using both accounts rather than choosing one over the other.

For years, financial discussions often framed retirement savings as a choice: Should you contribute to the Traditional TSP or the Roth TSP?

Today, another question deserves attention: If you’re already contributing to the Roth TSP, should you also open a Roth IRA?

The answer depends on your financial situation, eligibility, retirement goals, and tax planning strategy. Although both receive after-tax contributions and both can provide tax-free qualified distributions, Congress created them under different sections of the Internal Revenue Code. As a result, they have different eligibility rules, contribution limits, withdrawal rules, and long-term planning opportunities.

Understanding those differences can help federal employees make more informed retirement decisions.

Understanding the Difference Between a Roth TSP and a Roth IRA

One of the biggest misconceptions among federal employees is that a Roth TSP is simply a government version of a Roth IRA.

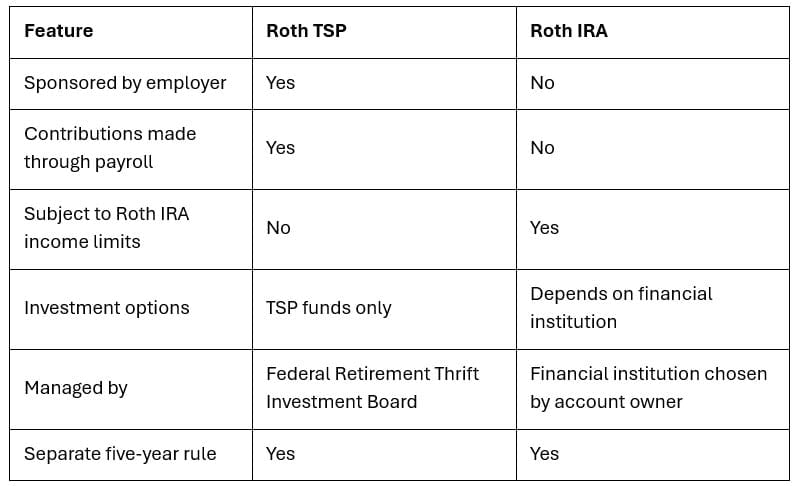

The Roth TSP is an employer-sponsored retirement plan administered by the Federal Retirement Thrift Investment Board. A Roth IRA is an individual retirement account established with a financial institution. While they share certain tax characteristics, they are governed differently.

Roth TSP vs. Roth IRA

Because they are separate accounts, one does not automatically replace the other. For many federal employees, each serves a different purpose within an overall retirement strategy.

Why Opening a Roth IRA Earlier Can Be Beneficial

One of the strongest reasons to open a Roth IRA before retirement has little to do with investments. It has to do with time. Specifically, the IRS five-year aging requirement. Many federal employees don’t discover this rule until they are preparing to retire. By then, valuable time may already have been lost.

Simply opening a Roth IRA and making an eligible contribution begins the account’s five-year aging period. Even a relatively small initial contribution can establish that starting point. Years later, that early decision may provide greater flexibility when managing retirement assets.

Understanding the Roth IRA Five-Year Rule

The IRS allows qualified Roth IRA withdrawals to be received tax-free when certain conditions are satisfied. One requirement is that the Roth IRA must satisfy its five-year aging requirement.

Generally speaking, the five-year period begins on January 1 of the tax year for which the owner’s first Roth IRA contribution or conversion is made. For example:

- Sarah opens her first Roth IRA in November 2026.

- She makes a contribution designated for tax year 2026.

- Her five-year period begins January 1, 2026 — not the day she opened the account.

This is why retirement professionals often encourage eligible individuals to establish a Roth IRA sooner rather than later, even if they cannot contribute large amounts initially. Time — not contribution size — is what starts the clock.

The Roth TSP Has Its Own Five-Year Rule

Another area of confusion involves the Roth TSP. Many people assume that satisfying the Roth TSP’s five-year rule automatically satisfies the Roth IRA’s rule. But these are separate retirement accounts with separate five-year requirements. Likewise, opening a Roth IRA does not retroactively satisfy the Roth TSP’s requirements.

Because the rules are independent, understanding how each account is treated can become especially important when planning retirement withdrawals or future rollovers.

SECURE 2.0 Act Changed in Lifetime Required Minimum Distributions

For years, one significant advantage of Roth IRAs over Roth TSP accounts involved Required Minimum Distributions (RMDs).

Before 2024, Roth TSP participants generally had to begin taking RMDs after reaching the applicable age unless they were still employed or rolled the money into a Roth IRA.

That changed with the SECURE 2.0 Act. Beginning in 2024, designated Roth accounts in employer retirement plans — including the Roth TSP— are no longer subject to lifetime Required Minimum Distributions while the funds remain in the plan.

This eliminated one of the largest planning differences between the Roth TSP and Roth IRA. Although that change narrowed the gap between the two accounts, other important differences remain — including investment flexibility, contribution eligibility, and the separate five-year aging rules.

Why This Still Matters

Because Roth TSP accounts are no longer subject to lifetime RMDs, some federal retirees may decide to leave their Roth money inside the TSP indefinitely. Others may still prefer moving assets into a Roth IRA after retirement because of broader investment options, estate planning preferences, or account consolidation. Neither approach is universally better.

The appropriate decision depends on each retiree’s financial objectives, investment preferences, and overall retirement income plan.

Rolling Your Roth TSP into a Roth IRA

Many federal employees eventually ask what happens to their Roth TSP after they retire or leave federal service.

In many cases, eligible participants may choose to leave the money in the TSP, roll it into another eligible employer plan that accepts Roth balances, or complete a direct rollover to a Roth IRA.

A direct rollover generally allows qualified Roth TSP assets to move into a Roth IRA without creating taxable income because taxes have already been paid on Roth contributions. However, the transaction should be completed as a direct rollover to avoid unnecessary complications.

It’s also important to understand that rolling Roth TSP money into a Roth IRA does not erase or restart the Roth IRA’s existing five-year aging period. If you’ve already established a Roth IRA, that account continues under its own timeline established by the IRS.

This is one reason some retirement professionals recommend opening a Roth IRA years before retirement, even if only a small annual contribution is made while you’re eligible.

More Investment Flexibility

One of the TSP’s greatest strengths is its simplicity. Participants can invest in a limited menu of professionally managed, low-cost funds that cover the major segments of the financial markets. For many federal employees, those options are more than sufficient to build a diversified retirement portfolio.

A Roth IRA, however, often provides access to a much broader range of investments depending on the financial institution where it is held. Those options may include:

- Individual stocks

- Corporate and municipal bonds

- Mutual funds

- Exchange-traded funds (ETFs)

- Certificates of deposit (CDs)

- Treasury securities

- Other investments offered by the IRA custodian

More investment choices are not automatically better. A larger selection also requires more research, monitoring, and discipline.

Many retirees appreciate the TSP’s straightforward investment menu and exceptionally low administrative expenses. Others prefer the flexibility available through a Roth IRA. The best choice depends on an individual’s investment knowledge, objectives, and comfort level.

Contribution Rules Are Different

Another significant difference involves who can contribute.

Anyone eligible to participate in the TSP may choose Traditional contributions, Roth contributions, or a combination of both through payroll deductions. Roth IRA contributions, however, are subject to annual IRS income limits.

Depending on your modified adjusted gross income (MAGI) and tax filing status, you may:

- Be eligible to contribute the full annual amount.

- Be eligible to contribute a reduced amount.

- Not be eligible to contribute directly to a Roth IRA for that tax year.

These income limits are adjusted periodically by the IRS. Federal employees whose income exceeds the limits may wish to discuss available retirement planning strategies with a qualified tax professional. While the IRS permits certain Roth conversions, those transactions involve separate rules beyond the scope of this article.

Using Both Accounts Together

For many federal employees, the question isn’t whether to choose the Roth TSP or a Roth IRA. It’s whether both accounts can complement one another.

A common approach looks like this:

Step 1: Contribute enough to the TSP to receive the full FERS agency matching contribution.

Step 2: If eligible under IRS rules, contribute to a Roth IRA.

Step 3: If additional retirement savings are available, continue increasing TSP contributions within annual IRS limits.

This strategy allows employees to take advantage of employer matching while also establishing a Roth IRA that may provide additional flexibility later in retirement. Of course, every financial situation is different. Contribution priorities may vary depending on age, income, debt, retirement goals, and other financial obligations.

Example

David is a 42-year-old FERS employee. He contributes 10 percent of his salary to the Roth TSP and receives the full government matching contribution. After reviewing the IRS eligibility requirements, he opens a Roth IRA and contributes a modest amount each year. Twenty years later, when David retires, he has two separate sources of Roth retirement savings. He may decide to:

- Leave both accounts as they are.

- Roll his Roth TSP into his Roth IRA.

- Keep part of each account.

- Develop another withdrawal strategy based on his retirement income needs.

Because he opened the Roth IRA years earlier, its five-year aging requirement has long since been satisfied. Having both accounts provides him with additional flexibility rather than limiting his options.

Common Misunderstandings

“I already have a Roth TSP, so I don’t need a Roth IRA.”

Not necessarily. The two accounts serve different purposes and operate under different IRS rules. Many federal employees choose to maintain both throughout their careers.

“Opening a Roth IRA means I have to move my TSP.”

No. Opening a Roth IRA does not require transferring any money from your TSP. The accounts can exist independently for decades.

“The Roth TSP and Roth IRA have the same five-year rule.”

No. Each account has its own five-year aging requirement. Understanding those differences can become important when planning retirement withdrawals and rollovers.

“The Roth IRA is always better.”

Not necessarily. The TSP offers advantages that many private-sector retirement plans cannot match, including low administrative costs and straightforward investment options. For many federal employees, the ideal solution is using both accounts together rather than replacing one with the other.

Frequently Asked Questions

Can I contribute to both a Roth TSP and a Roth IRA in the same year?

Yes. If you meet the IRS eligibility requirements for Roth IRA contributions, you may contribute to both accounts during the same tax year. The contribution limits are separate.

Do I have to roll my Roth TSP into a Roth IRA after retirement?

No. You may choose to leave your Roth TSP in the TSP if you prefer and continue to follow TSP withdrawal rules.

Does the Roth TSP still have Required Minimum Distributions?

Beginning in 2024, designated Roth accounts in employer retirement plans, including the Roth TSP, are no longer subject to lifetime Required Minimum Distributions while the funds remain in the plan.

Is opening a Roth IRA enough to start the five-year clock?

Generally, yes. The IRS measures the Roth IRA’s five-year aging period beginning with the tax year of your first Roth IRA contribution or conversion. Eligibility requirements for qualified tax-free distributions must also be met.

Should every federal employee open a Roth IRA?

Not necessarily. A Roth IRA can be an excellent planning tool for many federal employees, but eligibility depends on IRS income rules, and the decision should fit within an individual’s overall retirement strategy.