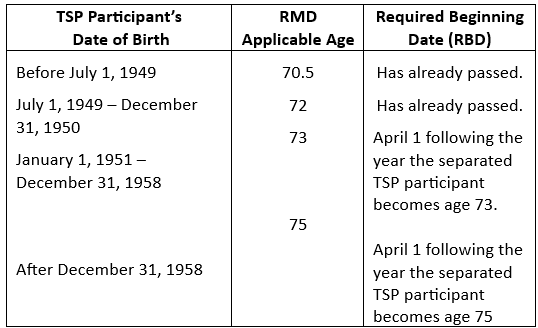

Retired Thrift Savings Plan (TSP) participants who retired from federal service either as a CSRS/CSRS Offset-covered employee or as a FERS-covered employee must begin receiving TSP required minimum distributions (RMDs) upon reaching their required beginning date (RBD).

The RBD depends on a retired TSP participant’s date of birth, as summarized in Table 1:

Table 1. RMD Applicable Age and Required Beginning Date (RBD) for a Retired TSP Participant*

*It is assumed that the retired TSP participant retired before they reached their RBD. A TSP participant who continues working in federal service past their RBD will then have an RBD of April 1st following the year that they retire.

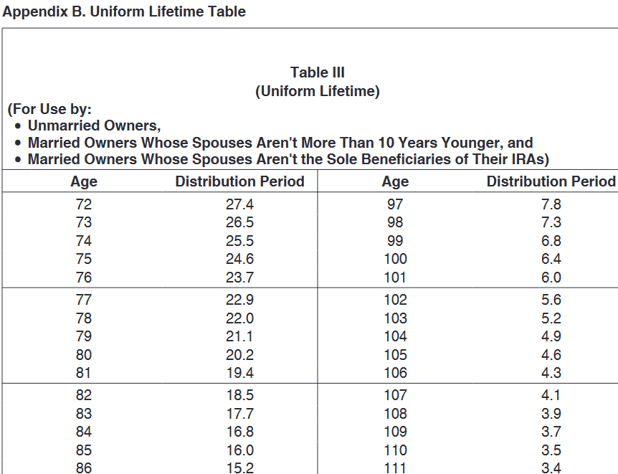

Prior to January 1, 2024, a retired TSP participant’s entire TSP account (consisting of both the participant’s traditional TSP account and the participant’s Roth TSP account) was used in the calculation of the annual TSP RMD. However, a provision coming out of SECURE Act 2.0 (2022) resulted in removing the Roth TSP in the calculation of the TSP RMD. Effective January 1, 2024, only the traditional TSP account is used in the calculation of the annual TSP RMD. Roth TSP account funds therefore are distributed as part of TSP participant’s annual RMD. The TSP Service Office calculates the TSP RMD each year that a TSP participant is required to receive a TSP RMD, using the TSP participant’s age, end of the prior year (December 31) traditional TSP account balance and the IRS’ Uniform Lifetime Table III found in Appendix B of IRS Publication 590-B (Distributions from Individual Retirement Arrangements). A portion of the Uniform Lifetime Table III is shown below.

The first year in which a TSP participant is separated and has reached their RBD is called the TSP participant’s first distribution year. Note that if a TSP participant continues in federal service past his or her RBD, then the RBD becomes April 1 following the year he or she retires from federal service. The following two examples illustrate:

Example 1. Jason was born September 15,1951 and retired from federal service in 2021. His RBD is April 1st following the year he became 73, which was 2024. Jason’s first distribution year was therefore 2024.

Example 2. Helen was born October 30,1949 and continued in federal service past her RBD of April 1st following the year she reached her RBD (which was April 1,2022). She retired from federal service on December 31, 2024. Her RBD is April 1,2025 That is because Helen’s first TSP distribution year is 2024.

The deadline for receiving the TSP RMD for the second and subsequent distribution year is not April 1 of the following calendar year. The deadline of April 1st of the following calendar year is only for the first distribution year. After the first distribution year, the deadline for receiving TSP RMDs is December 31st of the same (calendar) year.

The TSP will make sure that a TSP participant who has reached their RBD will meet the annual RMD requirement. In particular, if a TSP participant does not withdraw a sufficient amount of money from their traditional TSP account during the first distribution year, then the TSP will automatically (usually no later than March 15th of the following year) disburse money from the TSP participant’s traditional account to meet the first year RMD. Starting in the second distribution year, the deadline for meeting the annual TSP RMD is December 31st of that year. If a TSP participant subject to RMD has not withdrawn a sufficient amount of TSP money by December 1st, then the TSP will automatically (usually no later than December 15th) disburse money from the TSP participant’s traditional TSP account in order to meet that year’s RMD requirement.

How the Different TSP Withdrawal Options Meet the First Distribution Year RMD Requirement

As discussed in previous MFR columns, there are three methods by which a TSP participant can make withdrawals from their traditional TSP account. Each withdrawal method is reviewed together and how the method meets the first distribution year RMD requirement, together with what the TSP Service Office does in case the withdrawal method results in an insufficient amount of withdrawn traditional TSP monies to satisfy the TSP RMD for the first distribution year.

• Installment payments. A TSP participant’s installment payments count towards satisfying their first year RMD. If the amount of the installments (combined with any distributions that the TSP may make during the first distribution year) do not meet the first distribution year TSP RMD amount, then the TSP will automatically make a disbursement from the participant’s TSP account(s) in March of the following year in order to satisfy the TSP participant’s first year RMD requirement before the April 1 deadline. The following example illustrates:

Example 3. Angela retired from federal service March 31, 2022. She was born on October 25, 1950. Angela’s RBD is April 1 following the year she becomes age 72 (2022), or April 1, 2023. Her TSP account consisted only of traditional TSP. Her TSP account balance as 12/31/2021 was $783,900. Since Angela became age 72 during 2022, her first year TSP RMD for year 2022 must be taken by April 1, 2023. The TSP calculated Angela’s 2022 TSP RMD as follows:

$783,900 (account balance as 12/31/2021)/27.4 (life expectancy factor for a 72-year-old) = $28,610

Angela had requested from the TSP that starting July 1,2022, she receive a fixed monthly payment of $4,500 from her TSP account. From July 1,2022 through December 31, 2022, Angela received a total of 6 months times $4,500 per month, or $27,000. Angela notified the TSP in early December 2022 to cease the monthly installment payments as of January 1, 2023.

Because Angela was $28,610 less $27,000 or $1,610 short in her first distribution year TSP RMD requirement, the TSP on March 12,2023 withdrew $1,610 from Angela’s traditional TSP account and sent her a check. The TSP did this in order to make sure that Angela satisfy her first distribution year (2022) TSP RMD by the April 1,2023 deadline.

•Partial distribution. A TSP participant’s partial distribution will satisfy his or her first year TSP RMD if the distribution is at least the amount of the TSP participant’s first distribution year RMD.. If the partial distribution, combined with any subsequent distributions the TSP participant may make during the first distribution year do not meet the first distribution year TSP RMD, then the TSP will automatically send in March of the following year a supplemental payment to satisfy the TSP participant’s first distribution year TSP RMD before the April 1 deadline. The following example illustrates:

Example 4. Allan retired from federal service in 2024. He was born February 10, 1951. Allan’s RBD is April 1 following the year he became age 73 (2024), or April 1, 2025. His TSP account consisted of only his traditional

TSP balance as of 12/31/2024($669,700). Alan’s first year (2024) TSP RMD is calculated as follows:

$669,700 /26.5 (life expectancy factor for a 73-year-old) =$25,272

During 2024, Allan requested two partial distributions from his TSP accounts. One partial distribution on March 15,2024 was for $10,000, and one partial distribution on September 15,2024 was for $12,000. The two partial

distributions totaled $10,000 plus $12,000 or $22,000. That is all that Allan withdrew from his TSP account during 2022.

Since Allan was $25,272 less $22,000 or $3,272 short on his 2024 TSP RMD, the TSP on March 12, 2025 withdrew $3,272 from Allan’s TSP account and sent the $3,272 payment to Allan. They did this to make sure

that Allan fulfilled his first year TSP RMD by the April 1,2025 deadline.

• Annuity purchase. If a TSP participant purchases a TSP annuity during his or her first distribution year, then the TSP will send the TSP participant a separate check for the TSP participant’s full first year TSP RMD amount before processing the annuity purchase. The following example illustrates:

Example 5. Catherine retired from federal service in 2021. She was born April 17, 1950. Catherine’s RBD is April 1 following the year she became 72 (2022) or April 1, 2023. Her TSP account balance, consisting only of the traditional TSP, as of 12/31/2021 was $932,465. Catherine’s first year (2022) TSP RMD is calculated as follows:

$932,465 (account balance as of 12/31/2021)/27.4 (life expectancy factor for a 72-year-old) = $34,032

In November 2022, Catherine requested that the TSP purchase a $100,000 TSP annuity. Before the TSP processed Catherine’s TSP annuity request, the TSP withdrew $34,032 from Catherine’s TSP account and sent her a check, thus fulfilling Catherine’s first distribution year TSP RMD.

What Happens During the Second and Subsequent Distribution Calendar Years

Since the deadline for a TSP participant’s first distribution year is April 1 of the second distribution year, the TSP will continue to follow the rules explained above for the first two months of the second distribution year until the first year TSP RMD requirement has been met. A TSP participant’s second year distribution will not count toward the second year’s TSP RMD until the first year’s RMD is satisfied. If that first year TSP RMD requirement is not met by mid-March of the second year, then the TSP will automatically send the TSP participant what remains of the first year TSP RMD.

After the first year TSP RMD requirement has been met, the TSP participant’s subsequent distributions during the second year will count towards the second year TSP RMD requirement using the same rules described above for the first distribution calendar year, with two exceptions:

• December 31 deadline. After the first distribution year, the deadline for a given year’s RMD is December 31 of that year. That is, if a TSP participant subject to RMD has not satisfied his or her RMD by December 1, then the TSP will automatically send the TSP participant that year’s TSP RMD during early December of that year.

• Treatment of annuity purchases. The rule about sending a TSP participant an RMD check before processing any withdrawal request (including a TSP annuity purchase) no longer applies after a TSP participant has satisfied the first year’s RMD. If a TSP participant subject to RMD purchases a TSP annuity after the first distribution year annuity purchase will satisfy a portion of the RMD for that year in the following way: The percentage of the TSP participant’s account that is used to purchase the annuity is the same percentage of the TSP participant’s RMD that the TSP annuity purchase will satisfy. The following example illustrates:

Example 6. Harold, aged 75 during 2023, is a retired TSP participant. His TSP account consists of traditional TSP funds. His TSP account balance as of 12/31/2022 was $832,740. In January 2023, Harold received a notice from the TSP that his 2023 TSP RMD is equal to:

$832,740 (account balance as 12/31/2022)/24.6 (life expectancy factor for a 75-year-old) = $33,851

On April 5, 2023, Harold goes online to his TSP account and requests that the TSP use $100,000 of Harold’s TSP account to purchase a TSP annuity. Harold is therefore using $100,000/$832,740, or 12 percent of his TSP account to purchase his annuity. This means that Harold’s $33,851 TSP RMD for 2023

12 percent of $33,851 equals $4,062 has been satisfied by the TSP annuity purchase.

Harold will need to withdraw the remaining $33,851 less $4,065 equals $29,786 before December 31,2023 in order to satisfy his 2023 TSP RMD.

RMDs from Beneficiary TSP Participant Accounts

Beneficiary TSP participant accounts are also required to take RMDs. A beneficiary TSP participant is a TSP account in which a spouse beneficiary of a deceased civilian or a Uniformed Services TSP participant has a TSP account established in their name. As with civilian and Uniformed Services accounts, RMDs from beneficiary TSP accounts currently apply to both traditional and Roth TSP accounts. Effective January 1, 2024, RMDs for all TSP participant accounts apply only to a traditional TSP account.

For beneficiary TSP participant accounts, the TSP calculates any RMDs to be paid in the yar of the TSP participant’s death using the deceased TSP participant’s prior year-end TSP account balance, and the IRS’ Uniform Lifetime life expectancy table (see above). In the years following the deceased participant’s death, the TSP calculates the amount of the RMD using the beneficiary TSP participant’s age, prior year-end TSP account balance, and the IRS Single Life Expectancy Table, found in IRS Publication 590-B (Distributions from Individual Retirement Arrangements).

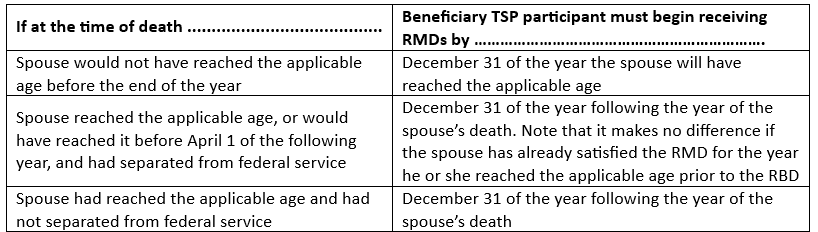

The date in which a beneficiary TSP participant must begin receiving RMDs depends on when the TSP participant died; namely – before or on/after their RBD. See Table 1 above which shows the RBD for individuals depending on when they were born. Note that Table 1 shows the “applicable age” which a beneficiary TSP participant will need to know if his or her spouse died before the RBD.

TSP Participant’s Date of Death is Before RBD

Table 2 below shows three possible scenarios in which a TSP participant (the “spouse”) died before his or her RBD and the deadline at which the beneficiary TSP participant must begin receiving RMDs:

Table 2. Beneficiary TSP Participant’s RMD Deadlines When Spouse Dies before His or Her RBD

Note that in the three scenarios presented in Table 2, the beneficiary TSP participant must continue to receive distributions by December 31 of each subsequent year. The TSP will base all of the beneficiary TSP participant’s RMDs on his or her age and not on the age of the deceased spouse.

TSP Participant’s Date of Death is On or After RBD

If a spouse dies after his or her RBD, then the deadline for the beneficiary participant’s RMD will depend on whether the spouse (the TSP participant) satisfied the RMD for the year of death.

• If the RMD for the year of death had been met, then the beneficiary TSP participant’s first RMD is due December 31 of the year following the year of the spouse’s death, and it is calculated based on the beneficiary TSP participant’s age, not the spouse’s age.

• If the RMD for the year of death had not been met, then the beneficiary TSP participant still needs to receive that RMD by December 31 of the year of death. In this case, the RMD is calculated based on the spouse’s age.

In both situations, the beneficiary TSP participant will need to make an RMD based on their age, (not the spouse’s age) by December 31 of each subsequent year.

TSP RMD Guide Booklet

For detailed rules regarding RMDs see the TSP guide, Tax Rules about TSP Payments(PDF 437kb).

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019