The release of the 2026 Medicare Trustees Report provides an early look at where Medicare costs may be headed in 2027. While the Centers for Medicare & Medicaid Services (CMS) will not announce official 2027 Medicare premiums, deductibles, and Income-Related Monthly Adjustment Amount (IRMAA) brackets until late 2026, the Trustees Report offers valuable projections that can help retirees and pre-retirees prepare.

For federal retirees and employees approaching retirement, understanding these projections is important because Medicare premiums can significantly affect retirement income planning.

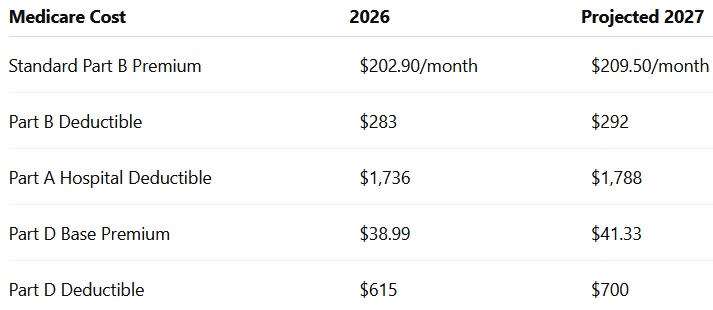

Projected Medicare Part B Premium for 2027

According to the 2026 Medicare Trustees Report, the standard Medicare Part B premium is projected to increase from $202.90 per month in 2026 to approximately $209.50 per month in 2027. This represents an increase of about 3.3%.

The Trustees Report projects that Part B premiums will continue rising over the coming decade as Medicare spending increases due to:

- Higher healthcare utilization

- Rising medical costs

- Increased enrollment from the aging population

- Growth in outpatient and physician services covered under Part B

Beneficiaries should remember that Medicare Part B premiums are designed to cover approximately 25% of total Part B program costs, with the remaining costs funded through general federal revenues.

Other Projected 2027 Medicare Costs

The Trustees Report and related Medicare projections indicate the following estimated 2027 costs:

These figures remain projections until CMS publishes official rates in the fall of 2026.

Why Some Retirees Will Pay Higher Medicare Premiums in 2027

Understanding the Income-Related Monthly Adjustment Amount (IRMAA)

Many Medicare beneficiaries pay only the standard Part B premium. However, higher-income retirees may be subject to the Income-Related Monthly Adjustment Amount (IRMAA).

IRMAA is an additional surcharge applied to:

- Medicare Part B premiums

- Medicare Part D premiums

The Social Security Administration determines IRMAA based on a retiree’s Modified Adjusted Gross Income (MAGI) from two years earlier. For 2027 Medicare premiums, the government will generally review income reported on a retiree’s 2025 federal tax return.

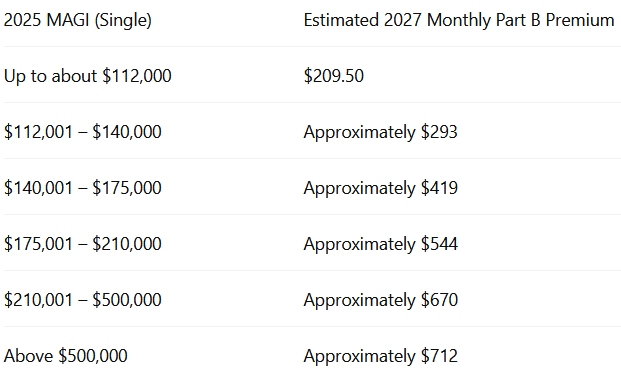

Projected 2027 IRMAA Thresholds

Because official 2027 IRMAA brackets have not yet been released, analysts have developed estimates based on inflation adjustments.

Current projections suggest the first IRMAA threshold may begin around:

- $112,000 MAGI for single filers

- $224,000 MAGI for married couples filing jointly

Income above those levels could trigger higher Medicare premiums in 2027.

Estimated 2027 Part B Premiums with IRMAA

Based on current projections, Medicare beneficiaries could pay the following monthly Part B premiums in 2027:

These figures are estimates and may change when CMS publishes final 2027 rates.

Why Retirement Income Planning Matters

For federal retirees with substantial retirement income, IRMAA can create a significant increase in healthcare costs.

Common sources of income that may increase MAGI include:

- Traditional IRA withdrawals

- Traditional TSP withdrawals

- Pension income

- Capital gains

- Rental income

- Large Roth conversions

A retiree who crosses an IRMAA threshold by even a small amount may move into a higher premium bracket for the entire year.

Planning Opportunities Before 2027

Because 2027 Medicare premiums will generally be based on 2025 income, retirees still have opportunities to manage future Medicare costs by:

- Monitoring taxable retirement account withdrawals.

- Coordinating Roth conversion strategies.

- Timing capital gains carefully.

- Reviewing required minimum distribution (RMD) impacts.

- Understanding how pension and Social Security income affect MAGI.

For many retirees, reducing IRMAA exposure can save thousands of dollars annually in Medicare premiums.