16 Things Seniors Born Between 1941-1969 Could Take Advantage Of

16 Things Seniors Born Between 1941-1969 Could Take Advantage Of

IRS Publication 559 (“Survivors, Executors and Administrators”) discusses how surviving family members, the Personal Representative or the Executor of the estate file the final federal income tax return for a family member who died during the current tax year. Filing a tax return for the year an individual dies presents some unique filing and reporting rules. This column discusses the rules for filing the federal income return (Form 1040) for an individual who died during 2025.

Filing Requirements for the Year of Death

A decedent’s tax year ends on the date of death. The due date of the decedent’s final Filing a tax return for the year an individual dies presents some unique filing and reporting rules. This column discusses the rules for filing the federal income return(Form 1040) for an individual who died during 2025 is the same as for individual s who lived the entire year. For example, if an individual died anytime between January 1 and December 31,2025, then the decedent’s 2025, then IRS Form 1040 must be filed by the income tax filing due date of April 15,2026, unless the executor or personal representative of his estate files for a six-month filing extension until October 15, 2026.

Normal tax accounting rules generally apply regarding the recognition of income and deductions, including the doctrine of “constructive receipt.” “Constructive receipt” is an accounting term that requires an individual to pay taxes on income despite the fact that the money has not yet been received in actuality.

The tax year of the federal estate income tax return (IRS Form 1041) begins the day after the deceased’s passing and must terminate at a month-end, no more than 12 months after the day of death. The estate may elect a fiscal year. The fiscal year does not have to coincide with the calendar year ending on December 31.

Who Can File the Decedent’s Final Federal Income Tax Return?

There are three individuals who can file the deceased’s final federal income tax return. They are the:

(1) Estate representative;

(2) Surviving spouse if the deceased was married at the time of death; or

(3) Person in charge of the decedent’s property. Each individual who is eligible to file on behalf of the deceased is discussed.

• Estate representative. If the decedent named an executor or if a court appoints a personal representative or other estate administrator, then that person is responsible for filing the return for the decedent. A joint tax return can be filed for a decedent and his or her surviving spouse if the spouse has not remarried by the end of the tax year, and the surviving spouse and estate representative agree that the deceased spouse and the surviving spouse should file jointly.

• Surviving spouse. If there is no court-appointed representative by the deadline for the return, then a surviving spouse who does not remarry before the end of the tax year can file a joint return with the decedent. A spouse can file a joint tax return even if he or she expects that an estate representative will be appointed. If the surviving spouse is the appointed representative, then he or she files for the decedent as representative and not as a surviving spouse.

• Person in charge of decedent’s property. If there are a court-appointed representative and no surviving spouse, then a person “in charge of the decedent’s property” must file the returns. This person may be anyone in actual or constructive possession of the decedent’s property, likely one of the heirs who is chosen informally by the other heirs to act in this capacity.

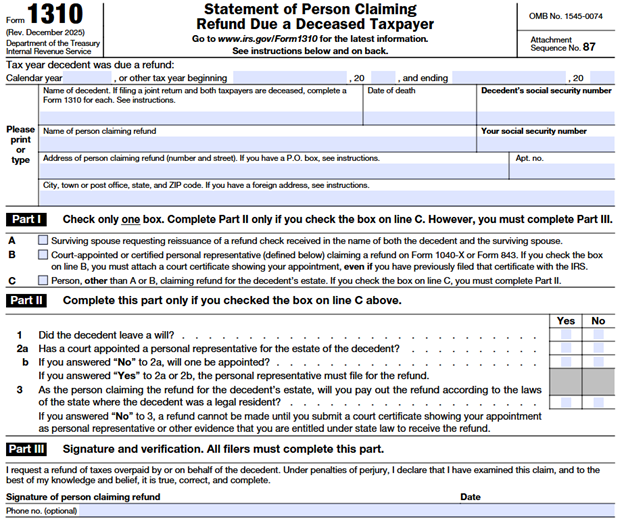

Filing by a person in charge of the decedent’s property should only be done for estates which will not require probate. If the tax return shows a refund, then the person chosen to file on behalf of the decent must verify on IRS Form 1310 (Statement of Person Claiming Refund Due a Deceased Taxpayer) that a court has not and will not appoint a personal representative. The IRS uses the term “personal representative” throughout Publication 559 and instructions to refer to both appointed representatives and persons in charge of the decedent’s property.

Reporting Income in the Year of Death

On the decedent’s final income tax return, the decedent’s includible income is generally determined as if the person were still alive. The only difference is that the taxable period ends on the day of death.

If the decedent accounted for income under the cash method (as most individuals do), then only those items actually or “constructively received” through from January 1 through the day of death are included in the final income tax return. The doctrine of “constructive receipt” requires a cash basis individual to recognize income when an item is credited to the individual’s account or made available without restricted filing. The following example illustrates:

Steven died on July 9, 2025. He had bond interest coupons that matured and became payable on June 30, 2025. Steven did not redeem these coupons before he died. Though he did not cash the coupons before he died, the interest income associated with the bond interest coupons must be included on Steven’s final Form 1040 because the income was available without restriction before he died.

In general, all income earned and paid until the day after the day of the decedent’s death needs to be reported on the decedent’s final Form 1040. This includes wage income, investment income (see below for specific information on how to report interest, dividend and capital gain income), pension and traditional IRA income, rental income and other income.

• Interest, dividend and capital gains distribution income. A Form 1099-INT and Form 1099-DIV should be received for the decedent. The 1099’s report interest and dividend/capital gain distributions earned before death and should be included on the decedent’s final income tax return. A separate Form 1099-INT and Form 1099-DIV should show the interest and dividends earned after the date of the decedent’s death and paid to the estate or other recipient and must include those amounts on the federal estate income tax return (IRS Form 1041). A Personal Representative or Executor should request corrected Form 1099’s from the payers if these forms do not properly reflect the correct recipient or amounts.

Note: It is challenging and often difficult to get the payers of interest, dividends, and capital gain distributions the information necessary to properly issue separate Form 1099s that apply to income earned from January 1 until the day of death and another set of 1099’s reporting income earned starting from the day after death until December 31. These payers include banks, brokerage firms, credit unions and the like. Therefore, a single Form 1099-INT and Form 1099-DIV may be received that includes all income for the year, before and after death. When that occurs, the Personal representative or Executor should follow the guides as reported in IRS Publication 559.

• Interest from US Savings Bonds. The personal representative or executor has three choices regarding the accrued interest on US Savings Bonds if the decedent never elected to report the US Savings Bond income as it accrued. These three choices are: (1) Report on the decedent’s final income tax return all interest earned before death. If the interest is not reported, then the income is “income in respect of a decedent” (IRD) and is not included on the decedent’s final return. The income is reported instead as interest income by the designated beneficiaries of the Savings Bonds when they redeem the bonds; (2) Report interest earned prior to death on the estate’s income tax return (IRS Form 1041); (3) If the personal representative or executor does nothing, the individual who redeems the savings bonds (the estate, an heir, or an assignee) must report the income on his or her federal income tax return.

Itemized Deductions in the Year of Death

Most rules for itemizing deductions (filing IRS Schedule A) for a decedent are the same as those for other individuals. When preparing their income taxes, individuals have the option of taking the standard deduction or itemizing allowed deductions. Allowable deductions are allowed if the expenses were paid prior to the decedent’s death (except for the special rule for medical expenses – see below) and would have been deductible by the decedent as of the date of death.

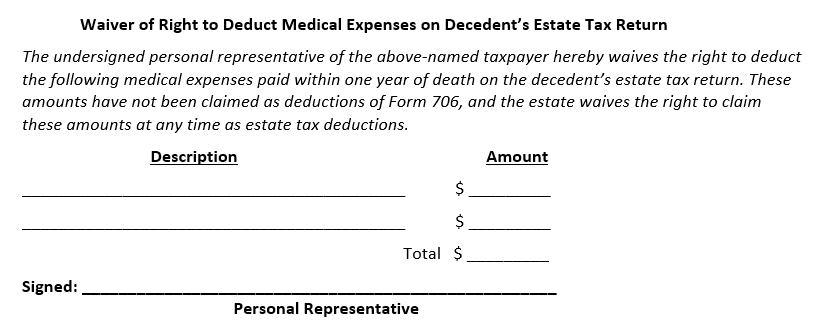

• Medical expenses. Medical costs paid from the decedent’s estate within one year of the day following death can be deducted either on Schedule A of the decedent’s Form 1040 or on the decedent’s Federal Estate Tax Return (IRS Form 706). If medical costs are deducted on the decedent’s Form 1040, they are deducted in the year incurred, either on the decedent’s final Form 1040 or by filing an amending Form 1040 from a prior year (Form 1040-X) and are subject to the 7.5 percent of adjusted gross income threshold. If the expenses are claimed on either Form 1040 or Form 1040-X, a waiver listing the expenses must be attached in duplicate to either return. The waiver is irrevocable. The statement is required even if the estate is not required to file IRS Form 706. The following is a sample waiver statement:

Taking the Standard Deduction in the Year of Death

The standard deduction can be claimed in full as if death had not occurred. A higher standard deduction for age is allowed if the deceased were aged 65 and/or older and/or blind during 2025. A decedent cannot use the standard deduction if the surviving spouse files separately and itemizes on the joint return.

Tax Credits in the Year of Death

Tax credits that applied to the decedent before death can be claimed on the decedent’s Form 1040. This includes the child tax credit, credit for the elderly or disabled, the earned income credit, and the adoption credit. Tax credits not used on the decedent’s final tax return will expire unused.

Note that if there are a surviving spouse and the decedent and surviving spouse file a joint tax return in the year of the spouse’s death, then any tax credit carried over is allocable to the surviving spouse and can be used by the surviving spouse in future years.

Other Final Federal Income Tax Return Filing Matters for An Individual Who Died During 2025

1. Tax return heading. The following should be written on the top of Form 1040: “DECEASED”, the decedent’s name, and the date of death across the income tax return. If it is a joint return – print the names, address and Social Security number of the decedent and surviving spouse as usual. If it is not a joint return – print the decedent’s name and Social Security number in the usual places. Print the name and address of the person filing the form in the remaining space.

2. Signing the return. The estate representative can sign the return. If there is a court appointed representative, then he or she must sign the return and include their title. If a joint return is filed, the representative signs for the decedent and the surviving spouse signs as usual, in the space for his or her signature. If there is no estate representative, the surviving spouse writes “Filing as Surviving Spouse” in the decedent’s signature space. The surviving spouse signs as usual in the space for his or her signature. The person in charge of the decedent’s property should sign his or her name followed by the words “Personal Representative.”

3. When and where to file. Regardless of when during 2025 death occurs, a decedent’s final income tax return is due at the same time the return would have been due had death not occurred. The due date of the final Form 1040 and Form 1041 for any individual who died during 2025 is April 15, 2026. Both Form 1040 and Form 1041 should be electronically filed and not mailed to the IRS.

4. Claiming a refund. If the 2025 federal income tax return shows a refund, IRS Form 1310 (see example below) or other documentation may be required depending on who files and signs the return.

5. Death certificate. The decedent’s death certificate or other proof of death should not be attached to the decedent’s final income tax return. It should instead be kept with the other decedent records and available upon request.

Federal employees or retirees who may have lost a relative during 2025 and who have questions about filing the tax returns on behalf of the decedent should consult with a knowledgeable tax professional. Also, if a decedent who died during 2025 lived in a state with a state and local income tax, state income tax returns will also likely need to be filed on behalf of the decedent.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019