Most federal employees and retirees receive some type of income that is not subject to mandatory federal and state withholding taxes. Among these types of income are investment income (interest, dividend and capital gain income), retirement income and IRAs, CSRS and FERS annuities, rental income and Social Security. But it makes no difference as to the type of income or the source of the income, the IRS wants to collect the tax due on income as soon as the income is received. This column discusses why some federal employees and retirees should make quarterly estimated tax payments to the IRS and, if they are residents of a state with an income to make quarterly estimated tax payments to their state revenue and tax departments.

It is important to explain the logic why individuals estimated tax payments. The US tax system works on a “pay-as-you-earn-basis.” That is why employers withhold federal and state income taxes, Social Security (FICA) and Medicare Part A (hospital insurance) payroll taxes from employee salaries. One goal of the US Treasury Department is to collect on a regular basis the taxes due on taxable income not subject to withholding. This is done through estimated tax payments. To accomplish this, the IRS has set up a timetable calling for estimated tax payments four times a year. Although the payments are commonly called “quarterly,” the payments do not coincide with calendar year quarters. The following table summarizes the “quarterly” income periods and due dates for the estimated tax payment for calendar year 2026.

The IRS recommends that individuals calculate the estimated tax liability amount for the entire calendar year, divide that amount by four and send in payments according to the schedule. There is a worksheet with the Form 1040-ES package or as part of most tax software packages such as Turbo Tax. The Form 1040-ES package can be downloaded by going to https://www.IRS.gov/pub/irs-pdf/f1040es.pdf.

A paper check along with the Form 1040-ES payment voucher can be sent to the IRS Service Center each quarter. Alternatively, an individual can file electronically with a credit card by enrolling in the IRS’ Electronic Federal Tax Payment System (EFTPS), or by using the IRS’ Direct Pay option.

There are incidences in which individuals may receive a “financial windfall and will spend the proceeds without setting aside some of the proceeds to pay estimated taxes. For example, during 2025 the stock market had a good year. Stock and stock mutual fund investors were the recipients of dividends, short and long-term capital gain income. This taxable income was paid to investors throughout 2025. There are unfortunately some investors who did not give much thought to paying estimated taxes throughout 2025, resulting in a huge federal income tax balance due (more than $1,000) and a possible federal income tax under withholding penalty when the 2025 federal income tax return is filed.

Ignoring one’s estimated tax responsibilities is not a wise tax move. In fact, if an individual owes more than $1,000 at the deadline for filing 2025 income taxes (this year, April 15, 2026), the individual could be subject to penalties and interest charges by the IRS, a result of federal income tax under withholding.

Determining Estimated Payments for 2026

The following are the steps employees and retirees should follow in determining how much to pay in Federal estimated tax payments during 2026. This procedure works even if an individual expects to owe substantially more in taxes during 2026 compared to what they owed during 2025. This is because the IRS considers that individuals are compliant when it comes to paying the required amount of federal income tax throughout the year (through payroll withholding and estimated tax payments) provided they pay either 90 percent of their current year (in this case, 2026) tax bill or a “safe harbor” payment based on either a 100 percent or 110 percent of the tax owed the previous year (in this case, 2025). The following are specific steps to determine how much an employee or a retiree should pay in federal estimated taxes during 2026:

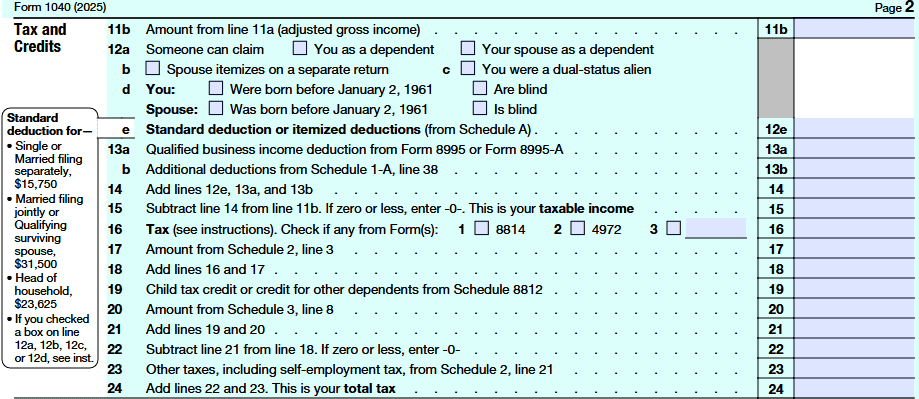

Step 1. Look at 2025 Form 1040, line 24 (total tax for 2025). See below. For example, suppose the total tax for 2025 is $21,500.

Step 2. Subtract from the amount in Step 1 the amount one expects to have withheld in Federal income taxes from wages, pensions, the TSP, IRAs, etc. during 2026. For example, suppose that amount is $18,500.

Step 3. Subtract the amount in Step 2 from the amount in Step 1. That gives the individual the amount to be made up through estimated tax payments. Divided the result by 4 and that is the amount that the individual pays to the IRS each quarter. In this example, $21,500 less $18,500 is $3,000; $3,000/4 or $750 is therefore the amount of the estimated tax payment each quarter throughout 2024 in order to eliminate any possible withholding penalty during 2026.

The IRS’ safe harbor for income tax withholding and estimated tax payments refers to a regulation that eliminates an individual’s liability as long as the individual acted in good faith. In the case of income taxes, it is an amount that protects the individual from IRS penalties for income tax underpayment.

For higher income individuals – individuals with previous year’s adjusted gross income (AGI) of more than $150,000 for married couples filing jointly and single individuals, ($75,000 for married individuals filing separately) the “safe harbor” percentage is increased to 110 percent of the previous year’s total tax.

Finally, federal employees can avoid paying estimated tax payments by filling out and submitting an updated W4 withholding form to their payroll office in order to request additional withholding. CSRS and FERS annuitants can request from OPM Federal and state income tax withholding from their annuities. They may do so by going onto their services online account with OPM. Social Security recipients can request Federal income tax withholding from their Social Security benefits. However, with nearly25 percent of calendar year 2026 having passed, some employees and annuitants may have to increase the amount of withholding by an additional 25 percent through the remainder of calendar year2026.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019