If eligible, a retiring CSRS or FERS employee may elect to receive the alternative form of a CSRS or FERS annuity (AFA). A retiring employee who elects and is accepted for the AFA will receive a lump sum payment equal to the employee’s contributions to the CSRS or FERS Retirement and Disability Fund. The retired employee also receives a reduced CSRS or FERS monthly annuity.

This column discusses the specific eligibility requirements for the AFA option, the calculation of the lump sum payment and reduced CSRS and FERS annuity, and the taxation of the lump sum payment and reduced CSRS and FERS annuity.

CSRS / FERS Lump Sum Annuity Eligibility

In order to be eligible for the AFA option, a retiring employee must meet all of the following requirements:

(1) Retire under the non-disability retirement rules;

(2) Have a life-threatening illness or other critical medical condition; and

(3) Not have a former spouse entitled to court-ordered CSRS or FERS annuity benefit based on an employee’s federal service.

A retiring employee who believes he or she is eligible for the AFA option because of a life-threatening affliction or other medical condition must attach a physician’s certification of his or her illness to the election. OPM will determine if the retiring employee is eligible for the AFA.

The following are examples of life-threatening conditions:

(1) Class IV – any physical activity that brings on discomfort and symptoms that occur at rest such as cardiac disease with congestive heart failure;

(2) Respiratory failure;

(3) Emphysema with respiratory failure;

(4) Cardiac aneurysm;

(5) active AIDS; and

(6) Aplastic anemia.

If a retiring employee elects and qualifies for an AFA, then the following applies:

1. A retiring employee’s CSRS annuity or FERS annuity will be permanently reduced. The reduction is determined by dividing the retiring employee’s lump-sum credit (see below) by an actuarial factor that depends on the retiring employee’s age.

2. The amount of any survivor annuity will not be affected.

3. An AFA retirement cannot be changed to a disability retirement after OPM processes the AFA retirement application.

4. When a retiring employee applies for the AFA retirement and receives the lump-sum payment, the retired employee will incur a federal and state tax liability for a portion of that payment.

Lump-Sum Payment and Federal Income Tax Liability

The lump-sum payment received under the AFA retirement option consists of a tax-free portion and represents a portion of the employee’s “cost basis” in the CSRS or FERS retirement. The “cost basis” includes employee payroll deductions into the CSRS or FERS Retirement and Disability Fund (deducted from after-tax salary), deposits for active military service, deposits for temporary service, and redeposits of withdrawn CSRS and FERS payroll contributions. Note that the employee contributions to the CSRS and FERS Retirement and Disability Fund, employee deposits and redeposits were made with after-tax funds. Therefore, this portion of the limp-sum payment is not taxable.

The taxable portion of the lump-sum payment consists of the total interest that has accrued on employee contributions to the CSRS and FERS Retirement fund, and on deposits and redeposits.

Generally, 80 to 90 percent of the lump-sum payment is taxable in the year it is received. A retiring employee can defer income tax by rolling over all or part of the payment to a traditional IRA, or another retirement plan that accepts rollovers. If the retired employee elects such a direct rollover, then taxes on the taxable portion of the lump-sum payment will be deferred until it is withdrawn from the traditional IRA or the retirement plan.

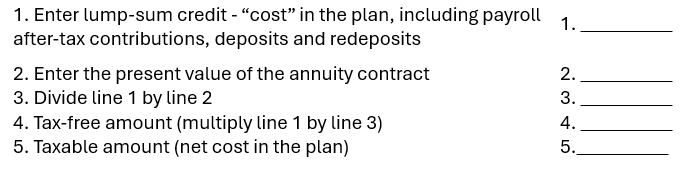

The following worksheet can be used to figure the taxable portion of the lump-sum payment:

Worksheet: Computing the taxable portion of lump-sum payment under the Alternative Annuity Option

Note that in order to complete the worksheet, a retiring employee needs to know the employee’s lump-sum credit and the present value of the contract. These terms are explained.

1. Lump-sum credit. Generally, this is the amount of an employee’s total contributions made via payroll deduction to the CSRS or FERS Retirement Disability Fund. These contributions were made with after-tax salary dollars. It also includes deposit and interest made (with after-tax dollars) by an employee for temporary (non-deduction) service and active-duty military service. Also included are redeposits including interest for any refunds of retirement contributions that a departed employee took when he or she initially left federal service and redeposited it when the departed employee returned to federal service. If an employee owes any deposits or redeposits for civilian service and elects the AFA option, then the deposits and redeposits are deemed to have been paid when computing the retirement benefit.

2. Present value of the annuity contract. The present value of the annuity contract is calculated using actuarial tables provided by the IRS. Those retiring employees who receive a lump-sum payment under the AFA option need to contact the IRS at the following address to find out the present value of their annuity contract:

Internal Revenue Service

Attention: Actuarial Group 2

TE/GE SE:T:EP:RA:T:A2

NCA-629

1111 Constitution Avenue, NW

Washington, DC 20224-0002

The following is an example.

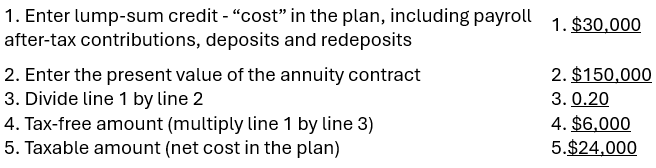

Steven retired from federal service under FERS in 2025, one month after his 60th birthday. He applied and qualified for the AFA option. During his 25 years of federal service, Steve had contributed $30,000 via payroll deduction to the FERS Retirement and Disability Fund. He qualified to receive a lump-sum payment under the AFA option. The present value of his annuity contract is $150,000.

The tax-free portion and the taxable portion of the lump sum are determined using the worksheet below:

Note from the worksheet:

(1) The tax-free portion (line 4) of the lump-sum payment is $6,000;

(2) The taxable portion (line 5) of the lump-sum payment is $24,000;

(3) Steven can request that OPM directly rollover the fully taxable $24,000 of the lump-sum payment into a traditional IRA. If Steven does this, then he will not pay income tax on the $24,000 until he withdraws the funds from the traditional IRA.

Those retiring employees who have chosen to receive a lump-sum payment under the AFA option will also receive a reduced CSRS or FERS monthly annuity. Those annuity payments will have a tax-free and a taxable portion. Under the Simplified Method, the tax-free portion of the monthly annuity is computed as discussed in a previous column, How CSRS and FERS Annuities are Taxed. However, the retired employee’s “cost” in the CSRS or FERS retirement will not include the lump-sum payment made under the alternative annuity option. For example, Steven’s “cost” in the FERS retirement will not include the $6,000 received tax-free as part of his lump-sum payment.

The AFA election does not affect the amount of a CSRS or FERS spousal survivor annuity. However, an AFA election does require the written consent of the retiring employee’s spouse. In the case of a former spouse who is entitled by a court order to a survivor annuity benefit, the law prohibits the election of an alternative form of annuity, even if the former spouse consents.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019