The countdown to the 2025 federal income tax return filing deadline is on. For individual income tax return filers, that deadline is April 15, 2026. With the deadline less than two weeks away, federal employees and retirees not only have a deadline to file their 2025 federal and state income tax returns, but also the deadline to make their 2025 IRA contributions.

April 15, 2026 is also the deadline for individuals who have not filed their 2022 federal income tax return to file their 2022 return in order to receive an expected refund. (Note that there is no statute of limitations for filing past-year returns if there is a balance due). This column discusses both of these deadlines.

Deadline to Make 2025 IRA Contributions

IRS rules allow IRA custodians to accept 2025 IRA contributions after April 15, 2026 if the contributions when mailed are mailed with a postmark of April 15, 2026 or earlier. This is the case even if the contribution does not reach the IRA custodian until after the April 15,2026 filing deadline has passed. IRA owners should also clearly indicate to their IRA custodians that their contributions are for tax year 2025 and not for tax year 2026. Failing to indicate that it is a 2025 IRA contribution may result in the IRA custodian reporting the IRA contribution as a 2026 IRA contribution. That could cause IRA problems for the IRA owner.

Three types of IRAs are available to federal employees and their spouses to make their 2025 IRA contributions. They are: (1) Deductible traditional IRAs; (2) Nondeductible traditional IRAs; and (3) Roth IRAs. Since federal employees are covered by a pension plan (CSRS or FERS) and they contribute to the Thrift Savings Plan (TSP), and most federal employee adjusted gross incomes are above the limits for contributing to a deductible traditional IRA, most federal employees are not eligible to contribute to a deductible traditional IRA. Therefore, only a nondeductible traditional IRA and a Roth IRA are discussed.

The maximum IRA contribution for 2025 is the lower of: (1) An individual’s earned income (wages/salary) and (2) $7,000 per individual for individuals younger than age 50 as of December 31, 2025, and $8,000 for individuals over age 49 as of December 31, 2025. For married individuals, both spouses can contribute the maximum to an IRA even if only one spouse has earned income – wages/salary or self-employment income with a net profit.

• Nondeductible traditional IRAs. Any individual with earned income – no matter their age or the amount of their adjusted gross income – can contribute to a nondeductible traditional IRA. With a nondeductible traditional IRA, there are no tax benefits when contributing because after-taxed dollars are used to contribute. The advantage of the nondeductible traditional IRA is that any earnings that accrue will not be taxed until the earnings are withdrawn after the IRA owner becomes 59.5. Note that contributions made to the nondeductible traditional IRA will not be taxed when withdrawn because these same contributions were made with after-taxed dollars. To make sure the IRS does not tax these contributions when they are withdrawn, the IRA owner must report their nondeductible traditional contributions on IRS Form 8606 (Nondeductible IRAs) for any year contributions are made to a nondeductible traditional IRA.

IRS Form 8606 is filed with one’s federal income tax return in any year the individual contributes to a nondeductible traditional IRA. If the individual has already filed his or her income tax return, then Form 8606 can be filed by itself with no penalty. Therefore, any employee who has already filed his or her 2025 federal income tax return can contribute to a nondeductible traditional IRA and report their contribution on 2025 Form 8606 separately with no penalty.

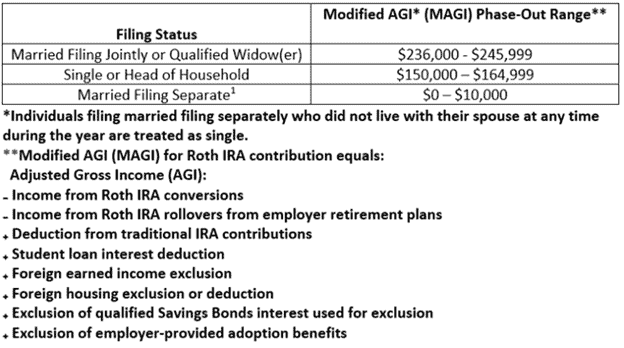

• Roth IRAs. With a Roth IRA, there is no paperwork (that is, no IRS forms) that has to be filed when an individual contributes to Roth IRA. Roth IRAs are beneficial because while there are no tax benefits when contributing to a Roth IRA, all qualified distributions from a Roth IRA are completely tax-free. All contributions are made with after-taxed dollars and earnings accrued tax-free. The only limitation associated with contributing to a Roth IRA is that there are modified adjusted gross income (MAGI) limitations for contributing to a Roth IRA. These income limitations for 2025 are presented in the table below.

Table 1. 2025 Roth IRA Modified Adjusted Gross Income (MAGI) Contribution Limitations

*See Worksheet 1 to determine Modified Adjusted Gross Income (MAGI)

**See Worksheet 2 to determine the reduced contribution amount.

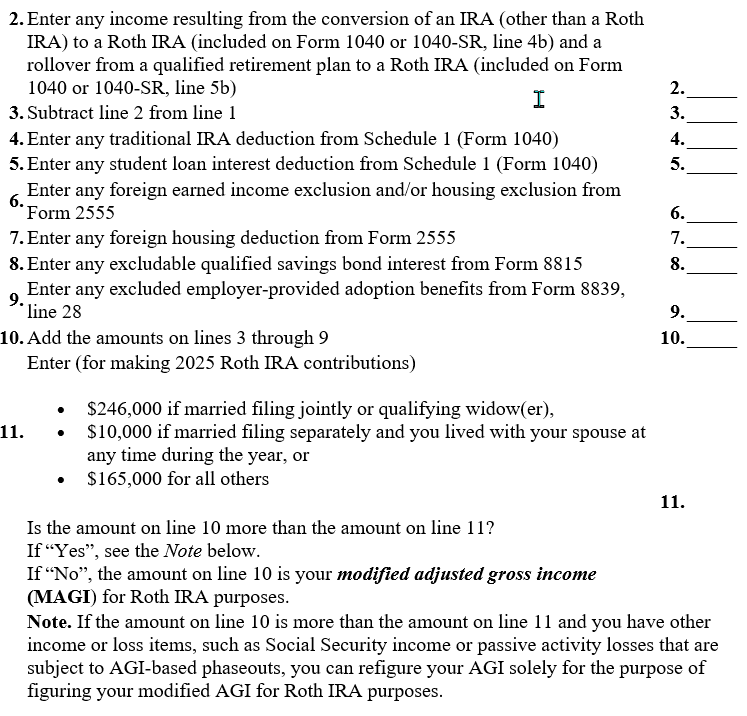

Worksheet 1. Modified Adjusted Gross Income (MAGI) for Roth IRA Contribution Purposes

Use this worksheet to figure your 2025 modified adjusted gross income for Roth IRA purposes.

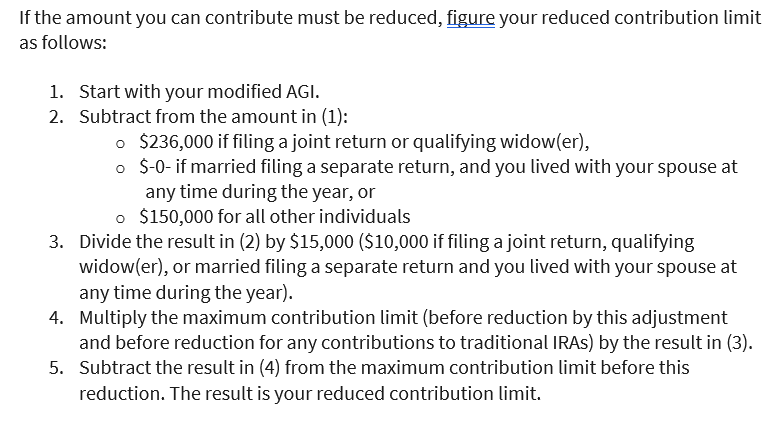

Worksheet 2. Reduced 2025 Roth IRA Contributions Based on 2025 Modified AGI

Any employee who previously contributed to a Roth IRA during calendar year 2025 but now discovers (due to higher-than-expected modified AGI) that he or she is not eligible to contribute to a Roth IRA for the year, can “recharacterize” their contribution to a nondeductible traditional IRA. The employee has until October 15,2026 to do so. To recharacterize the Roth IRA contribution, the Roth IRA owner must contact the Roth IRA custodian to remove the contribution and accrued earnings and transfer that amount to a nondeductible traditional IRA.

SEE ALSO: How to Recharacterize IRA Contributions

Filing Federal 2022 Income Tax Returns to Receive a Refund

The IRS recently announced that over 1.3 million people across the US have unclaimed refunds for tax year 2022. These individuals face an April 15, 2026 deadline to submit their 2022 federal income tax returns. The IRS estimates that approximately $1.2 billion in refunds remains unclaimed for taxpayers who have not filed their Form 1040 Federal income tax return for the 2022 tax year. The IRS estimates the median refund amount is $686 for 2022, which means that half of the refunds are more than $686. This estimate does not include credits that may be applicable.

Under the law, taxpayers usually have three years to file and claim their tax refunds. If they do not file within three years, the money becomes the property of the U.S. Treasury. To look a breakdown by state as to the estimated number of individuals who have not filed their 2022 federal income tax returns and median amount of their refunds, the median potential refund, and the total potential refunds go here.

The IRS reminds taxpayers seeking a 2022 tax refund that their funds may be held if they have not filed tax returns for 2023 and 2024. In addition, any refund for 2022 will be applied to amounts still owed to the IRS or a state tax agency and may be used to offset unpaid child support or other past due federal debts, such as student loan debts.

Current and prior year tax forms, such as the tax year 2022 Forms 1040 and 1040-SR, and instructions are available on the IRS.gov Forms & Instructions page or by calling toll-free 800-TAX-FORM (800-829-3676).

To obtain 2022 income and tax reporting documents, individuals have a few options. Although it has been a few years since 2022, the IRS reminds taxpayers that there are ways they can still gather the information they need to file the 2022 tax return. But individuals should ensure they have enough time to file before the April deadline for 2022 refunds. Here are some options:

• Request copies of key documents: Taxpayers who are missing Forms W-2, 1098, 1099 or 5498 for the years, 2022, 2023 or 2024 can request copies from their employer, bank or other payers.

• Use Get Transcript Online at IRS.gov. Taxpayers who are unable to get missing forms from their employer or other payers can order a free wage and income transcript at IRS.gov using the Get Transcript Online tool. For many taxpayers, this is by far the quickest and easiest option.

• Request a transcript. Another option is for people to file Form 4506-T with the IRS to request a “wage and income transcript.” A wage and income transcript shows data from information returns received by the IRS, such as Forms W-2, 1099, 1098, Form 5498 and IRA contribution information. Taxpayers can use the information from the transcript to file their tax return. Plan ahead, written transcripts requests using Form 4506-T can take several weeks. Individuals are strongly encouraged to try other options first.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019