Individuals with one or more qualifying children may be eligible to claim on their 2025 Federal income tax return a tax credit of up to $2,200 per child. This tax credit is called the child tax credit (CTC). The Taxpayer Relief Act of 1997 first introduced a nonrefundable CTC of $400 per qualifying child under age 17. The CTC slowly increased until the Tax Cuts and Jobs Act of 2017 (TCJA) which increased the credit to $2,000 and made up to $1,400 of the credit as refundable. Refundable tax credits reduce one’s tax liability dollar-for-dollar, and if the credit amount exceeds an individual’s tax liability, the IRS refunds the difference.

The CTC is generally a nonrefundable tax credit that is limited to an individual’s regular tax liability plus alternative minimum tax (AMT) liability.

OBBBA Changes to the Child Tax Credit

The one Big Beautiful Bill Act (OBBBA), which President Trump signed into law in July 2025, permanently extended the enhanced CTC beyond 2025. The CTC credit increased to $2,200 per qualifying child and indexed the $2,200 amount beginning in 2026. The credit for other dependents is $500 and was made permanent.

Who Is a Qualifying Child for the CTC?

The definition of a qualifying child for the CTC is the same as that for the dependent tax exemption except for the following:

‧ Age: Child must be under age 17; and

‧ Citizenship or resident: Child must be a US citizen, resident alien, or national.

A qualifying child must be claimed as a dependent and have a Social Security Number valid for employment issued by the Social Security Administration. An eligible individual seeking the CTC based on a qualifying child must include the child’s SSN on their federal income tax return.

Adjusted Gross Income (AGI) Phase-Out

The $2,200 CTC is “phased out” by $50 for each $1,000 or fraction thereof of an individual’s modified adjusted gross income (MAGI) above the beginning phase-out amount. The MAGI in which the credit is completely phased out depends on the number of qualifying children.

The phaseout amounts are $400,000 for married filing jointly and $200,000 for all other filers – single, head of household, married filing separately. These amounts will not be indexed for inflation. The MAGI phase-out rules also apply to the ODC. The following example illustrates:

Joan is a single parent with a 12-year-old daughter who is a qualifying child. She has a MAGI of $250,000. Before any phase-out, her CTC is $2,200. The phase-out reduction is computed as follows:

$250,000 MAGI less $200,000 threshold amount = $50,000

$50,000 above threshold amount: $50,000 /$1,000 = 50

50 x $50 = $2,500 reduction

Since the reduction amount of $2,500 exceeds the pre-phaseout credit amount of $2,200, Joan’s CTC for 2025 s $0.

Credit for Other Dependents (ODC)

A $500 credit is allowed for each dependent of an individual other than a qualifying child. The non-refundable credit applies to: (1) A child under age 19; (2) A full-time student under age 24; (3) A disabled child of any age; or (4) Other qualifying relatives. To qualify, an individual must be a US citizen, a US national, or a US resident.

Calculating the Child Tax Credit and the ODC

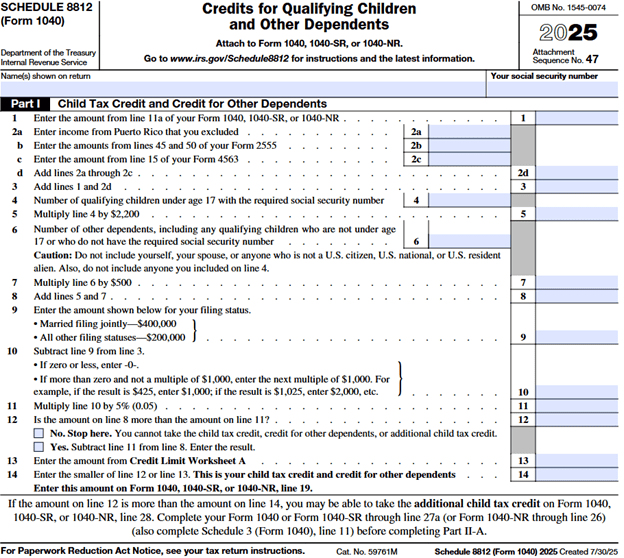

Individuals who are eligible for the CTC or the ODC must complete Part I of IRS Schedule 8812, Credits for Qualifying Children and Other Dependents. Part I of IRS Schedule 8812 is shown here:

For most individuals, the CTC is the smaller of: (1) $2,200 multiplied by the number of qualifying children less the applicable phase-out amount; or (2) Regular tax liability plus alternative minimum tax (AMT) liability reduced by the foreign tax credit and other nonrefundable personal tax credits, such as the child and dependent care, education and retirement savings credits.

Additional Child Tax Credit (ACTC)

A portion of the child tax credit is refundable for certain individuals. Individuals complete Part II of IRS Schedule 8812 to complete the refundable portion of the credit, called the additional child tax credit.

Note that the refundable portion of the ACTC for any qualifying child cannot exceed $1,700. The partial credit for other dependents is disregarded for this purpose.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER®, Chartered Life Underwriter, Chartered Financial Consultant, Registered Health Underwriter and Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, located at 833 Bromley Street Suite A, Silver Spring, MD 20902-3019