Many federal employees contribute to the Thrift Savings Plan (TSP) without fully understanding the differences between the G, F, C, S, I, and Lifecycle (L) Funds — or when to use each one.

This guide guide breaks down every TSP investment option, explains the Mutual Fund Window, and shows how investment elections, fund reallocations, and fund transfers really work.

Why the TSP Is a Powerful Retirement Savings Tool

The TSP offers several advantages that make it one of the lowest-cost retirement plans available.

These include:

- Automatic payroll deductions

- Traditional and Roth contribution options

- Professionally managed investment funds

- Lifecycle (L) Funds that automatically adjust over time

- The Mutual Fund Window for additional investment choices

- Extremely low administrative expenses

For most federal employees, consistently contributing to the TSP over a long career can become one of the largest sources of retirement income.

Understanding the Five Core TSP Funds

The foundation of the TSP consists of five core investment funds.

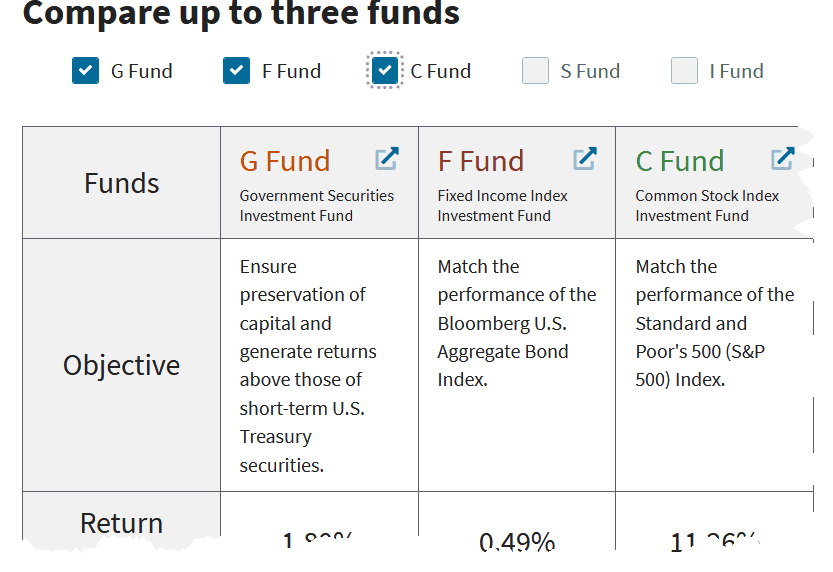

G Fund – Government Securities Investment Fund

The G Fund is unique because it invests in special U.S. Treasury securities issued specifically for the TSP.

Key characteristics include:

- Principal is backed by the U.S. Government.

- No risk of losing principal due to market fluctuations.

- Historically has earned returns that generally outpace inflation.

- Produces steady, relatively modest returns.

The G Fund is often considered the most conservative TSP investment option.

F Fund – Fixed Income Index Investment Fund

The F Fund tracks the Bloomberg U.S. Aggregate Bond Index.

It invests in:

- U.S. government bonds

- Corporate bonds

- Mortgage-backed securities

Compared to the G Fund, the F Fund generally offers higher return potential but also experiences price fluctuations as interest rates change.

C Fund – Common Stock Index Investment Fund

The C Fund follows the S&P 500 Index and includes approximately 500 of America’s largest publicly traded companies.

Examples include companies such as:

- Apple

- Microsoft

- Amazon

- Berkshire Hathaway

- Tesla

Historically, the C Fund has produced some of the strongest long-term returns in the TSP, although investors should expect market ups and downs along the way.

S Fund – Small Capitalization Stock Index Investment Fund

TheS Fund invests in thousands of smaller U.S. companies that are not included in the S&P 500. Because these companies tend to be smaller and faster growing, the S Fund has:

- Greater growth potential

- Higher volatility

- Larger price swings than the C Fund

Many long-term investors use the S Fund alongside the C Fund for broader U.S. stock market exposure.

I Fund – International Stock Index Investment Fund

The I Fund provides exposure to developed and emerging international markets outside the United States. Its investments include companies located throughout:

- Europe

- Japan

- Australia

- Other developed and emerging economies

Because it invests overseas, returns can be affected by:

- Foreign stock markets

- Currency exchange rates

- Global economic conditions

Adding international investments can help diversify a retirement portfolio.

TSP Fund Online Comparison Tool

Consider using the TSP’s online fund comparison tool.

What Are Lifecycle (L) Funds?

Not everyone wants to decide how much to invest in each individual fund. Each Lifecycle (L) Fund is professionally managed and contains a mix of the five core funds (G, F, C, S, and I). The allocation automatically becomes more conservative as the target retirement date approaches.

For example:

- L 2075 is designed for participants with many years before retirement and therefore holds a larger percentage in stock funds.

- L Income is designed for participants already in retirement or very close to retirement and holds much more in the G and F Funds.

Federal employees automatically enrolled in the TSP are generally placed into the L Fund that corresponds with their expected retirement timeline based on age. However, participants are not required to remain in that fund and may select a different L Fund if it better matches their personal risk tolerance.

Understanding Investment Risk

Every investment carries some level of risk. TSP participants should understand several common investment risks.

Credit Risk

The possibility that bond issuers fail to repay investors.

Present primarily in the F Fund.

Inflation Risk

The risk that investment returns fail to keep pace with rising prices.

This affects every investment option.

Market Risk

The possibility that stock or bond prices decline due to overall market conditions.

This applies to the F, C, S, and I Funds.

Currency Risk

International investments can gain or lose value as foreign currencies rise or fall relative to the U.S. dollar.

This primarily affects the I Fund.

Prepayment Risk

Mortgage-backed securities inside the F Fund may be paid off early when interest rates decline, potentially reducing investment returns.

What Is the TSP Mutual Fund Window?

Participants who want additional investment choices may use the Mutual Fund Window.

Important rules include:

- No more than 25% of your total TSP balance may be invested through the Mutual Fund Window.

- Your initial investment must be at least $10,000.

- Loans and withdrawals cannot be taken directly from assets held in the Mutual Fund Window. Funds must first be transferred back into the regular TSP investment funds.

The Mutual Fund Window offers expanded investment flexibility but may not be appropriate for every investor.

Understanding the Three Types of Investment Transactions

One area that often causes confusion is how TSP investment changes work. Here are the three different TSP investment transactions:

Investment Election

A TSP investment election changes future contributions only.

Money already invested remains exactly where it is.

Fund Reallocation

A TSP fund reallocation changes both:

- Existing account balances

- Future contributions

This effectively resets your entire investment allocation.

Fund Transfer

A TSP fund transfer moves only existing money between funds.

Future payroll contributions continue following your previous investment election unless you separately change them.

![]()

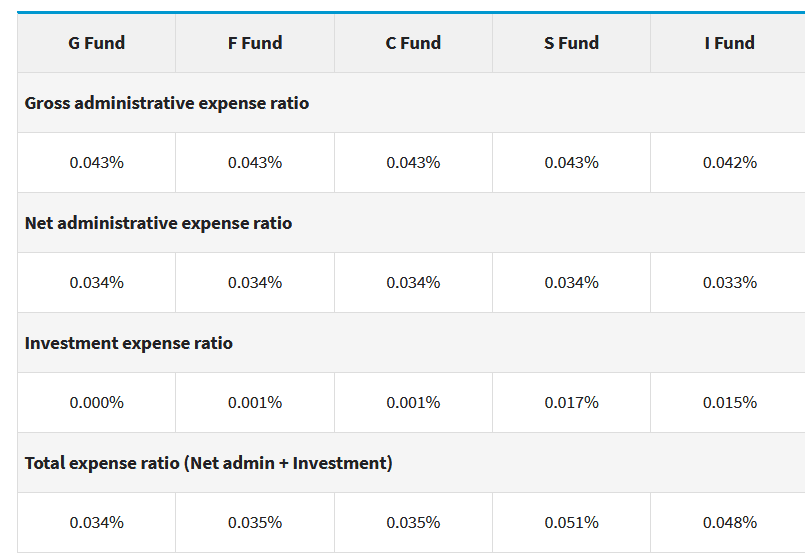

Keep an Eye on Investment Expenses

One of the biggest strengths of the TSP continues to be its exceptionally low expenses.

Expense ratios cover costs such as:

- Recordkeeping

- Account administration

- Participant services

- Statements and educational materials

These expenses remain significantly lower than those charged by many private-sector retirement plans and mutual funds, allowing more of your investment returns to remain in your account over time.